Quick Summary: In 2026-27, India’s GST system has become faster, smarter — and more unforgiving. The introduction of a Zero Mismatch Policy from April 2026, AI-driven scrutiny, and automatic ITC blocking means that small compliance errors now have immediate financial consequences.

This blog covers the 7 most painful GST problems businesses are facing right now, and exactly what to do about each one.

Why GST Compliance Has Become Harder — Not Easier — in 2026

When GST was introduced in 2017, the promise was simplification. One tax. One return. One portal. Eight years later, many businesses will tell you the reality feels different. The portal has improved, yes. But the system has also become far more aggressive about enforcing compliance — and far less tolerant of errors, even honest ones.

Here is what has changed: the GST portal now uses AI-driven reconciliation to cross-verify your GSTR-1, GSTR-3B, and GSTR-2B in real time. From April 2026, a Zero Mismatch Policy means the portal automatically blocks your return filing if your ITC claims do not match supplier filings — no manual overrides, no second chances. The GST department issued over 33,000 compliance notices in FY 2024-25 alone, most of them triggered by automated systems detecting discrepancies that taxpayers did not even know existed.

The businesses that suffer the most are not fraudsters. They are ordinary businesses with untrained accounts teams, unresponsive suppliers, outdated software, or simply too much volume to manually reconcile every invoice. Below are the seven problems hurting businesses most — and what to do about each one.

Pain Point 1 – ITC Mismatch Between GSTR-2B and GSTR-3B

What the problem looks like: Your business claims Input Tax Credit (ITC) for GST paid on purchases. But the portal cross-checks your claim against what your suppliers have actually uploaded in their GSTR-1. If there is a mismatch — even by a single invoice — the portal flags it. From April 2026, mismatched ITC is automatically blocked at source. You cannot file your GSTR-3B until the mismatch is resolved.

Why it happens: The most common reason is a supplier who filed their GSTR-1 late or incorrectly. If your supplier missed an invoice or entered the wrong GSTIN, that invoice does not appear in your GSTR-2B, and the ITC you legitimately paid is blocked. Other causes include timing differences (supplier filed in month 2, you claimed in month 1), incorrect GST rates entered by either party, and credit/debit notes not properly matched.

What to do: Reconcile your purchase register against GSTR-2B every month — before filing GSTR-3B. Do not claim ITC on invoices that are not in your GSTR-2B. For missing invoices, follow up with your suppliers immediately after the 11th of each month (when GSTR-1 is due). Build a supplier compliance tracker — rate your vendors by their GST filing consistency. Low-compliance vendors are costing you real money in blocked ITC and cash flow disruption.

If ITC is blocked due to a genuine supplier error, document the invoice, the payment, and your follow-up communication. This paper trail is essential if the matter goes to a notice or appeal.

Pain Point 2 – GST Portal Technical Glitches and Downtime

What the problem looks like: Every time a filing deadline approaches — GSTR-1 on the 11th, GSTR-3B on the 20th — the GST portal slows to a crawl or crashes entirely. Taxpayers and CAs trying to file legitimate returns at the deadline get error messages. And because the portal went down, they miss the deadline and incur late fees — for a failure that was not their fault.

Why it happens: India has over 1.5 crore GST-registered taxpayers. The vast majority of them attempt to file in the last 48–72 hours before a deadline. The portal’s servers, regardless of how they have been upgraded, face enormous concurrent load during these windows. The result is authentication failures, zero balances showing in credit/cash ledgers despite funds being available, and submission timeouts.

What to do: The single most effective fix is to not file at the last minute. If your GSTR-1 is due on the 11th, your data should be ready by the 8th, and you should file by the 9th. If your GSTR-3B is due on the 20th, reconcile and file by the 17th. Businesses that file early never experience portal downtime issues.

Use a professional CA or compliance firm to handle your returns on a fixed schedule, not a deadline-driven scramble. If you do face a portal error, take a screenshot with a timestamp immediately — this is your evidence if you need to request late fee waiver citing technical issues on the GSTN portal, which the department does accept in genuine cases.

Pain Point 3 – GST Notices and Automated Scrutiny in 2026

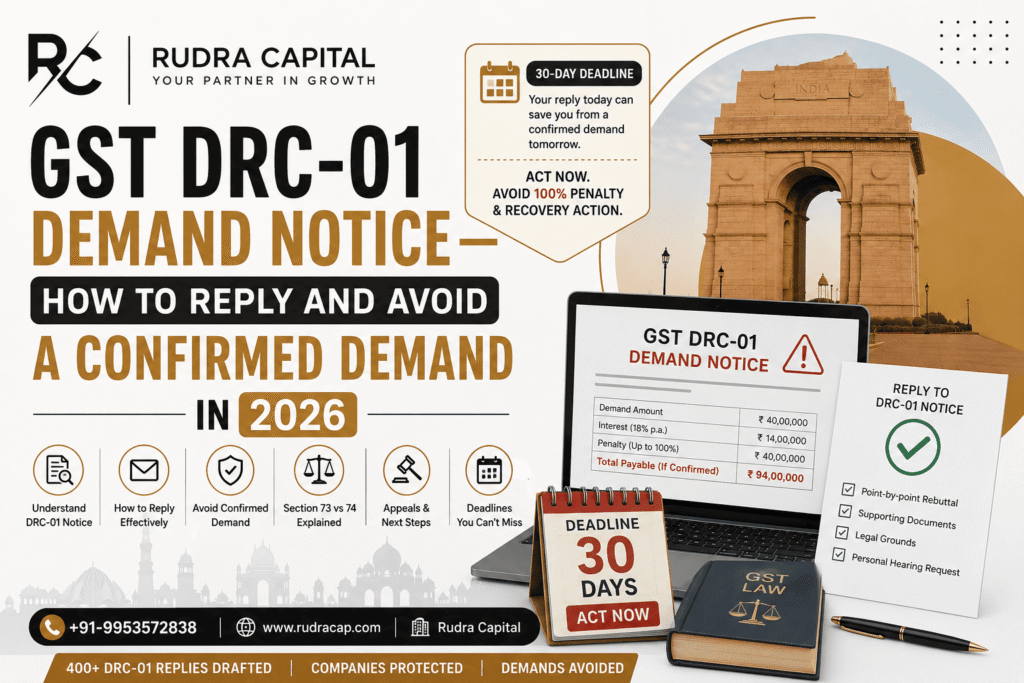

What the problem looks like: You receive a DRC-01A or DRC-01C notice from the GST department. The notice says there is a discrepancy between the tax you declared and the tax the system calculated. You have 7–15 days to respond. If you do not respond correctly and on time, a formal demand is raised — and you owe the tax amount plus interest at 18–24% per year plus penalties.

Why this is getting worse: The GST department has deployed AI-based analytics to identify mismatches between GSTR-1 and GSTR-3B, between declared turnover and e-invoice data, between GST paid and income tax turnover, and between ITC claimed and ITC eligible. In 2025, even a ₹5,000 mismatch can trigger an automated notice. The system does not distinguish between a genuine error and deliberate evasion.

Most common notice triggers:

- Outward supply declared in GSTR-1 does not match what is declared in GSTR-3B

- ITC claimed exceeds what is available in GSTR-2B

- Turnover in GST returns does not match the Income Tax return (cross-database matching)

- E-invoice data does not match GSTR-1 data

- GSTR-9 annual return figures differ from monthly return totals

What to do: Always reconcile GSTR-1 and GSTR-3B before filing. Never let a notice sit unanswered — the 7-15 day window is strict. A properly drafted response citing specific legal provisions (Section 16, Rule 88C, etc.) can resolve most automated notices without any tax demand. Engaging a GST professional for notice response is essential — an incorrect reply can escalate the matter rather than close it.

If you have received a GST notice, call Rudra Capital immediately at +91-9953572838. Do not ignore it or respond without expert guidance.

Pain Point 4 – Reverse Charge Mechanism (RCM) Confusion

What the problem looks like: Your business receives a service from an unregistered supplier — a freelance consultant, a small vendor, or a landlord renting commercial premises. Under the Reverse Charge Mechanism, you (the recipient) are required to pay GST directly to the government on their behalf, even though they did not charge it to you. Many businesses are unaware of this obligation, or aware of it but unsure which transactions it applies to.

Why it matters: Failure to pay RCM GST is treated as a compliance failure — and it attracts interest at 18% per year on the unpaid amount from the due date, plus penalties. The GST department’s audit teams specifically look for RCM compliance gaps, particularly in sectors like professional services, commercial rent, transportation, and goods imported through unregistered vendors.

Common RCM-applicable transactions businesses miss:

- Services from advocates (legal fees)

- Goods Transport Agency (GTA) services

- Rent paid to an unregistered landlord for commercial premises

- Sponsorship services

- Services from a director to a company in their personal capacity

- Import of services (any service received from outside India)

What to do: Maintain a register of all payments to unregistered vendors and identify which ones attract RCM. Set up a process to self-invoice for RCM transactions and ensure the GST is paid by the 20th of the following month. Your CA or compliance team should include an RCM check in the monthly GST review process.

Pain Point 5 – GSTR-9 Annual Return Complexity

What the problem looks like: The GSTR-9 annual return is meant to be a summary of the entire year’s GST transactions. In practice, it requires reconciling 12 months of GSTR-1, GSTR-3B, and purchase data, identifying any amendments made across the year, and declaring the exact ITC eligible vs. ITC claimed vs. ITC reversed. Getting all of this right in one form — while operating a business — is genuinely difficult.

The stakes in 2026: GSTR-9 for FY 2026-27 now has automatic late fees that increase every day you delay. If you have turnover above ₹5 crore, you also need to file GSTR-9C (reconciliation statement with certification). Errors in GSTR-9 that contradict your monthly returns attract notices and adjustment demands.

Common mistakes in GSTR-9:

- ITC figures in GSTR-9 do not match GSTR-3B totals

- Amendments and credit notes not properly accounted for

- RCM paid during the year not reflected correctly

- Differences between GST turnover and Income Tax turnover not explained

What to do: Start preparing for GSTR-9 from the beginning of the financial year, not in December or January. Maintain a running annual reconciliation register throughout the year. Engage a professional for GSTR-9 filing — this is not a return that should be self-filed without expert review.

Pain Point 6 – E-Invoice and E-Way Bill Errors

What the problem looks like: E-invoicing is mandatory for businesses with annual turnover above ₹5 crore. The Invoice Registration Portal (IRP) assigns a unique Invoice Reference Number (IRN) and QR code to each invoice. If the invoice data — GSTIN, HSN code, tax rate, place of supply — contains even a small error, the IRP rejects the invoice. Meanwhile, your e-way bill may have different details from your invoice, causing issues at checkposts.

Common e-invoice and e-way bill errors:

- Incorrect or missing HSN codes (the portal requires 4-digit or 6-digit HSN depending on turnover)

- Wrong place of supply leading to wrong tax type (IGST vs CGST+SGST)

- GSTIN of buyer entered incorrectly

- E-way bill not generated or generated after goods have already moved

- Mismatch between e-invoice and e-way bill data

Consequences: A rejected IRN means the invoice is not valid for the buyer to claim ITC. An e-way bill with wrong details can lead to seizure of goods in transit, a GST demand on the full value of the consignment, and penalties under Section 129 of the CGST Act.

What to do: Use ERP or accounting software that is integrated with the IRP and generates e-invoices automatically with validated data. Train your billing team on HSN codes applicable to your products/services. Always generate the e-way bill before goods leave your premises. Reconcile e-invoice data against GSTR-1 before filing.

Pain Point 7 – Late Fees, Interest, and Penalty Accumulation

What the problem looks like: A business misses a GSTR-3B deadline in April. Late fee is ₹50 per day. They are busy and miss May too. By June, they owe ₹9,000 in late fees across two returns before paying any tax. Then they discover they also have interest on the unpaid tax at 18% per annum. By the time they try to regularise, the total liability has become substantial — and it is all because of a missed date, not fraudulent evasion.

Late fee rates (as of 2026):

- GSTR-3B: ₹50/day (₹20/day for nil returns), capped at ₹10,000 per return

- GSTR-1: ₹50/day (₹20/day for nil returns), capped at ₹10,000 per return

- GSTR-9: ₹200/day (₹100 CGST + ₹100 SGST), no cap — this can become very large

- Interest on unpaid tax: 18% per annum from the due date

What to do: Never let GST returns accumulate as pending. If cash flow is tight and you cannot pay the full tax, file the return anyway with a partial payment — this stops the late fee clock. The interest will still run on the unpaid amount, but stopping the late fee accumulation alone saves significant money. Set up calendar reminders for all GST due dates. Consider appointing a professional compliance firm to manage your GST calendar and ensure nothing is missed.

How Rudra Capital team helps you???

The businesses that face the fewest GST problems are not the ones with the most complex tax situations — they are the ones with the most organised compliance processes.

At Rudra Capital, we provide end-to-end GST compliance support:

- Monthly GSTR-1 and GSTR-3B filing with prior reconciliation

- ITC reconciliation against GSTR-2B every month before filing

- GST notice drafting and response — DRC-01, ASMT-10, and other notices handled by our CA team

- GSTR-9 and GSTR-9C preparation with annual reconciliation

- E-invoice and e-way bill setup and support

- RCM compliance tracking and self-invoice management

Our clients do not miss deadlines, do not accumulate late fees, and receive notice alerts with expert response support the moment an issue arises.

To get your GST compliance on track, call us at +91-9953572838 or book a free strategy call.

FAQs on GST Issues in 2026

Q1: What is the penalty for late GSTR-3B filing? The late fee is ₹50 per day (₹20 per day for nil returns), capped at ₹10,000 per return. Additionally, interest at 18% per annum applies on any unpaid tax amount from the original due date.

Q2: How do I resolve a GSTR-2B vs GSTR-3B ITC mismatch? First, identify the specific invoices causing the mismatch. For supplier errors, follow up with the vendor to file a corrected GSTR-1. For your own errors, adjust in the next GSTR-3B. Maintain a reconciliation file as documentation. For large amounts, consult a CA before making adjustments.

Q3: I received a DRC-01A notice. What do I do? Do not ignore it. You have a limited window to respond. Draft a written response citing the specific reason for the discrepancy — whether it is a supplier filing delay, a timing difference, or an error now corrected. Attach supporting documents. An incorrect or non-response can result in the tax demand being confirmed with penalties.

Q4: Is the Zero Mismatch Policy in effect right now? Yes. From April 1, 2026, the GST portal automatically blocks ITC claims that do not match supplier filings. Manual overrides for mismatched claims are no longer possible.

Q5: Do I need to file GSTR-9 even if my turnover is below the threshold? GSTR-9 is mandatory for businesses with annual turnover above ₹2 crore. For those below ₹2 crore, it is optional. However, GSTR-9C (reconciliation statement) is required only if turnover exceeds ₹5 crore.

Struggling with GST compliance? Rudra Capital’s GST team handles your returns, reconciliation, and notice responses — so you can focus on your business. Call +91-9953572838 or contact us here.