Written by the CA & GST Advisory Team, Rudra Capital — handling GST notice responses, revocation applications, pending return filings, and GSTIN reactivation for businesses across Delhi NCR. Our team has successfully revoked over 150 suo moto cancellations.

Last reviewed: May 2026 | References: Section 29(2) CGST Act 2017 · Rule 20–23 CGST Rules · GST Portal REG-17, REG-21, REG-22, REG-23 · Finance Act 2023 (extended revocation window to 90 days) · CBIC Circular 158/14/2021

GST Registration Cancelled by Department? How to Revoke It and Get Your GSTIN Back

Covers: Why GST is cancelled suo moto · Immediate consequences · Voluntary vs suo moto distinction · 90-day + 270-day windows · Step-by-step REG-21 process · REG-23 response strategy · Fresh registration if window missed

Covers: Why GST is cancelled suo moto · Immediate consequences · Voluntary vs suo moto distinction · 90-day + 270-day windows · Step-by-step REG-21 process · REG-23 response strategy · Fresh registration if window missed

If your GST registration has been cancelled — stop, read this first.

From the moment your GSTIN is cancelled, every invoice you raise is legally invalid. Every ITC your customers claim on your invoices is at risk. You cannot file returns, collect GST, or claim existing credit ledger balances. And critically: you have a fixed window — 90 days without condonation, 270 days maximum — to reverse this. Every day of delay shrinks your options.

This guide tells you exactly what happened, exactly what it means for your business, and exactly what steps to take — in the right order, with the right forms — to get your GSTIN reactivated as fast as possible.

Why Does the GST Department Cancel Registrations Suo Moto?

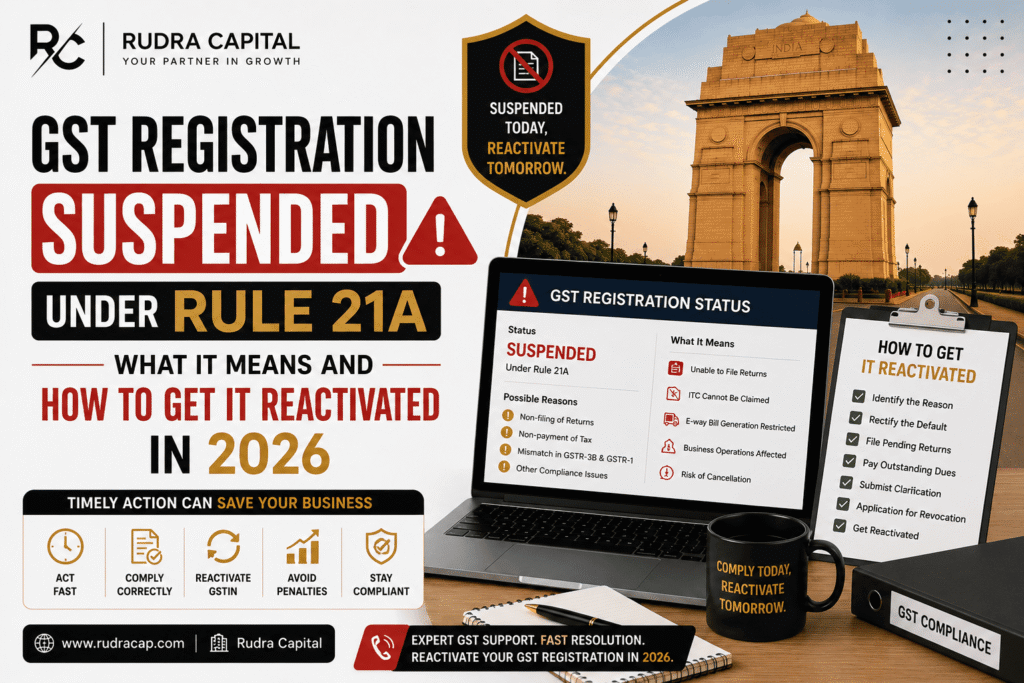

The GST department cancels a registration on its own motion — without any application from you — under Section 29(2) of the CGST Act. This is called suo moto cancellation, and it is the only type that can be reversed through the revocation process.

The most common reasons for suo moto cancellation in 2026:

Reason 1 — Non-filing of GSTR-3B for 6+ consecutive months (most common)

The GST portal’s automated system monitors return filing patterns. If a regular taxpayer does not file GSTR-3B for 6 consecutive months, the system initiates a show cause notice in Form GST REG-17. If you do not respond within 7 working days, the cancellation order in Form GST REG-19 is issued.

Reason 2 — GSTR-1 not filed for 2 consecutive quarters (QRMP filers)

Taxpayers on the Quarterly Return Monthly Payment (QRMP) scheme who miss two consecutive quarterly GSTR-1 filings trigger the same cancellation process.

Reason 3 — Business found non-existent during field verification

If a GST officer visits the registered address during a physical verification drive and finds the business is not operational there — or finds significant discrepancies between the declared and actual nature of business — proceedings can be initiated.

Reason 4 — Fraudulent ITC claims or fake invoice network

AI-driven analytics identify circular invoicing patterns, fake ITC claims, and round-tripping. These result in immediate cancellation combined with recovery proceedings — the most serious category, requiring legal assistance beyond ordinary revocation.

Reason 5 — Database cleansing (registration with no business activity)

Periodically, the GST department runs cleansing drives to remove GSTINs registered by businesses that never commenced taxable supplies. These cancellations are challengeable if the business was genuinely operational.

The most important question to ask first: Was your cancellation suo-moto (department-initiated) or voluntary (you applied for it using Form REG-16)? Only suo-moto cancellations can be revoked. If you voluntarily surrendered your GSTIN and now want it back, you must apply for fresh registration — revocation is not available. Check your cancellation order: if it cites REG-19 issued by a proper officer (not in response to your application), it is suo-moto and revocable.

The most important question to ask first: Was your cancellation suo-moto (department-initiated) or voluntary (you applied for it using Form REG-16)? Only suo-moto cancellations can be revoked. If you voluntarily surrendered your GSTIN and now want it back, you must apply for fresh registration — revocation is not available. Check your cancellation order: if it cites REG-19 issued by a proper officer (not in response to your application), it is suo-moto and revocable.

The Immediate Consequences of a Cancelled GSTIN

Understanding what your cancelled GSTIN means in practice is essential to appreciating the urgency of acting quickly:

| WHAT YOU CANNOT DO??? | BUSINESS IMPACT |

|---|---|

| File any GST return | Compliance gap grows; late fees and penalties accumulate daily |

| Raise valid tax invoices | Every invoice raised during cancellation period is invalid under Rule 46. Customers cannot claim ITC. |

| Use credit ledger ITC balance | ITC balance is blocked — cannot be utilised for output tax payment |

| Claim GST refunds | Pending refund applications are suspended |

| Operate as a GST-registered supplier for B2B customers | GSTIN status shows “Cancelled” on the portal — buyers’ due diligence fails; orders at risk |

The Revocation Windows — 90 Days, 270 Days, and What Happens After

Under the CGST Rules as amended by the Finance Act 2023, the revocation timeline for suo moto cancellations is:

0–90

Days from cancellation order

File REG-21 directly. No condonation needed. Cleanest and fastest path.

91–270

Days from cancellation order

File REG-21 with condonation of delay. Explain why you could not apply within 90 days. Officer has discretion.

271+

Days from cancellation order

Revocation not possible. Must apply for fresh GST registration. Old GSTIN and credit ledger balance are permanently lost.

✓ How to find your cancellation date: Log in to GST portal → Services → My Registrations. Look for the registration status showing “Cancelled.” Click on the GSTIN to view the cancellation order. The order will show the date of cancellation — this is day zero for your 90-day and 270-day calculations. Also check whether the cancellation date on the order matches the date the status changed on the portal.

Step 1 — File All Pending GST Returns Immediately

The GST portal will not accept your Form REG-21 revocation application until every pending GSTR-1 and GSTR-3B return has been filed. This prerequisite is enforced at the portal level — there is no bypass.

This step is typically the most time-consuming part of the revocation process. Here is how to approach it efficiently:

Return Filing Sequence

1

Log in to GST portal → Returns → Returns Dashboard. Note the earliest period with a pending GSTR-1 — this is where you begin. The portal requires chronological filing; you cannot file June before filing April.

2

For each period, file GSTR-1 first (even if nil), then GSTR-3B. A nil GSTR-1 takes under 5 minutes. A substantive GSTR-1 requires your invoice data — prepare this in advance before sitting down to file.

3

While filing GSTR-3B, compute the tax liability for each period and pay via the cash ledger if the credit ledger is blocked. Late fees (₹50/day GSTR-3B + ₹50/day GSTR-1, capped at ₹10,000 each per return) are also payable — calculate the total before starting so you have sufficient funds available.

4

Note the acknowledgement number for every return filed. These become exhibits in your REG-21 application. File through the current period — even if the cancellation happened 18 months ago, file every single pending return.

The accumulated late fee reality: If your cancellation followed 12 months of non-filing, your total late fee exposure before penalty (6 months GSTR-3B × ₹10,000 cap + 6 months GSTR-1 × ₹10,000 cap) can be ₹1,20,000 or more. Calculate this before starting and ensure you have sufficient cash available to pay all outstanding liabilities — the portal will not allow return filing without payment of dues.

Step 2 — Pay All Outstanding Tax, Interest, and Late Fees

Step 1 and Step 2 are intertwined — as you file each pending return, the associated tax, interest (18% per annum from original due date), and late fees must be paid. The portal calculates the interest automatically when you attempt to file.

For a business with 9 months of non-filing and ₹2 lakh average monthly GST liability:

Estimated outstanding liability calculation

Tax (9 months × ₹2L)

₹18,00,000

Interest @18% p.a. (avg 5 months lag)

~₹1,35,000

Late fees (capped ₹10K × 9 × 2 returns)

₹1,80,000

Total estimated outflow

~₹21,15,000

Note: Actual amounts depend on your specific tax liability, credit available, and exact delay period. This illustration shows why early revocation (within 90 days) is far less costly than delayed action.

Step 3 — Submit Form GST REG-21 on the Portal

Once all pending returns are filed and all dues are paid, you can apply for revocation using Form GST REG-21:

REG-21 Filing Process — Step by Step

1

Log in to gst.gov.in → Services → Registration → Application for Revocation of Cancellation of Registration. This option only appears for cancelled GSTINs where the cancellation was suo moto.

2

In the “Reason for Revocation” field, write a clear, factual explanation: (a) why returns were not filed — business disruption, health emergency, management difficulties; (b) what steps have been completed to rectify compliance — all pending returns filed, all dues paid; (c) your commitment to maintaining compliance going forward.

3

Attach supporting documents as exhibits: acknowledgement numbers of all freshly filed returns; challan receipts for all dues paid; any documentary evidence for the reason for default (medical records, business closure notice, etc.).

4

Sign using DSC (for companies/LLPs) or EVC (for individuals and proprietorships). Submit. Note the Application Reference Number (ARN) — you will receive an acknowledgement on your registered email and mobile.

5

Track application status at: GST Portal → Services → Registration → Track Application Status. Enter the ARN to see current status.

Step 4 — Responding to Form GST REG-23 (If the Officer Issues a Query)

After you submit REG-21, the proper officer has 30 days to either approve (Form GST REG-22 — revocation order) or query (Form GST REG-23 — show cause notice on revocation application).

If you receive REG-23, it means the officer is not fully satisfied with your revocation application and is asking specific questions or requesting additional documentation. You have 7 working days to respond in Form GST REG-24.

✓ How to draft a strong REG-24 response:

- Address every query in the REG-23 specifically — do not give generic answers

- If the officer questions whether the business was genuinely operational, attach current proof: GST invoices, bank statements showing business transactions, utility bills for the business premises, photographs of business activity

- If the officer questions the reason for non-filing, provide concrete documentary evidence (medical certificates, insolvency proceedings against a key partner, documented business disruption)

- Request a personal hearing if the REG-23 raises complex factual issues — a conversation is sometimes more effective than a written response alone

If the officer is satisfied with REG-24, they issue Form GST REG-22 — the revocation order. Your GSTIN is restored to active status. If not satisfied, they issue Form GST REG-05 (rejection order). You can appeal against REG-05 to the Appellate Authority under Section 107 of the CGST Act within 3 months.

Condonation of Delay (91–270 Days) — What Changes

If you are between day 91 and day 270 from the cancellation date, your revocation application requires an additional element: a formal explanation of why you could not apply within the primary 90-day window.

The condonation application is included within the REG-21 form itself — there is a specific field for “Reason for applying beyond 90 days.” The officer uses this explanation to exercise discretionary approval. To maximise your chances:

- Be specific about the reason for delay — “I was unaware” is weak; “I was hospitalised from [date] to [date], documentary evidence attached” is strong

- Document all compliance now completed: returns filed, dues paid, interest paid, late fees settled

- Show that the business is active and will remain compliant: current customer invoices, active bank account showing business transactions, any renewed registrations or licences

- Business disruption during COVID-19 (FY 2019-20 to 2021-22) has been accepted by most GST authorities as valid condonation reason, but supporting documentation is still needed

After 270 Days — Fresh Registration Is Your Only Option

If the 270-day window has passed without a successful revocation, the old GSTIN cannot be restored. The only path forward is applying for fresh GST registration, which means:

- New GSTIN: A completely new GST registration number, not connected to the old one

- ITC balance lost: Any credit balance in the old registration’s credit ledger is permanently forfeited — it cannot be carried to the new registration

- Clean compliance start: The new registration starts fresh with no default history — but the old GSTIN’s cancelled status remains on the department’s records

- Customer impact: All existing customers who have your old GSTIN in their vendor master must be updated with the new GSTIN; past invoices under the old GSTIN cannot be amended

✓ The cost of waiting: Every day between cancellation and action increases your penalty liability, shrinks your revocation options, and damages your business relationships. The cost of filing all pending returns and paying dues within the first 90 days is almost always less than the cost of managing a fresh registration with lost ITC and disrupted customer relationships. The urgency is real.

GST registration cancelled? Every day counts — call Rudra Capital now.

Our GST team handles the complete revocation process — pending return filing for all periods, dues calculation, REG-21 application drafting, REG-23 response, and post-revocation compliance setup. We have successfully revoked over 150 suo moto cancellations across Delhi NCR.

FAQs — GST Registration Cancellation and Revocation

Related reading: GST Show Cause Notice Reply · GST Pain Points 2026 · GST Registration Service