Written by the Tax Litigation, Assessment & Pre-Scrutiny Advisory Team, Rudra Capital — advisors who have represented mid and large Indian companies before Assessing Officers, CIT(A), ITAT, and High Courts in income tax, GST, TDS, and transfer pricing disputes; designed pre-litigation tax defense frameworks for 120+ companies; and conducted over 200 pre-scrutiny tax health audits that identified and resolved material risks before they became notices.

Last reviewed: June 2026 | References: Income Tax Act 1961 (Sections 131, 142, 143, 147, 148, 148A, 156, 270A, 271, 276C) · GST Act 2017 · Finance Act 2025 · CBDT Annual Report 2024-25 · CBDT Project Insight Guidelines · CBDT Enhanced Scrutiny Guidelines 2025 · ITAT Annual Statistical Report 2024-25

For CFOs, Business Owners, Finance Directors, and Legal Heads of mid and large Indian companies — listed and unlisted. Covers: how a tax notice becomes a financial crisis · the 8-stage escalation from query to High Court · the 10 most common CBDT notice triggers in 2026 · the true total cost of a ₹10 crore demand · 7 warning signs your company is already on CBDT’s radar · CBDT’s 2026 enforcement priorities · the six-pillar pre-litigation defense framework · How Rudra Capital helps · 8 expert FAQs

For CFOs, Business Owners, Finance Directors, and Legal Heads of mid and large Indian companies — listed and unlisted. Covers: how a tax notice becomes a financial crisis · the 8-stage escalation from query to High Court · the 10 most common CBDT notice triggers in 2026 · the true total cost of a ₹10 crore demand · 7 warning signs your company is already on CBDT’s radar · CBDT’s 2026 enforcement priorities · the six-pillar pre-litigation defense framework · How Rudra Capital helps · 8 expert FAQs

March 2025. A listed mid-cap manufacturing company in Pune receives a notice under Section 148A of the Income Tax Act. The company had a respected CA firm filing its returns. It had passed statutory audit for three consecutive years without qualification. Its MD believed the company’s tax affairs were clean. The CBDT notice claimed that ₹14.2 crore in income had escaped assessment — citing cash purchases from vendors with no GST filing history, related-party loan transactions at below-market interest rates, and unexplained bank credit entries across two assessment years. The company had 30 days to respond.

The CA firm that filed the returns had never handled a Section 148A notice at this scale. They responded with factually accurate but legally thin boilerplate — a response that failed to address the specific evidentiary basis for CBDT’s allegation. CBDT issued a Section 148 show cause notice three weeks later. By month six, the Assessing Officer had raised a demand of ₹9.2 crore. By month twelve, CIT(A) had confirmed ₹7.4 crore. The company filed an ITAT appeal. Total timeline so far: three years and ongoing. Advisory fees paid: ₹46 lakh. Senior management time diverted from operations: over 380 hours. The notice that arrived in March 2025 — for a company that believed its tax affairs were clean — is still not resolved.

This guide is built around one central question: does your company have the structures, documentation, and advisory relationships in place to ensure that the next notice CBDT sends you does not become what happened to that Pune manufacturer? Because in 2026, the question is not whether your company will receive a CBDT notice. The question is whether you will be ready — with documentation, a response protocol, and specialist representation — when it arrives.

The 2026 tax litigation landscape: As of March 2026, CBDT’s Annual Report shows more than ₹35 lakh crore in disputed direct tax demands pending across all stages of appeal in India. Over 5.4 lakh cases are pending at CIT(A) level alone. The average time from Section 148A notice to final ITAT order: 4.5 to 7 years. In 2025-26, CBDT processed 1.8 lakh scrutiny assessments — with mid and large companies accounting for over 70% of total demand raised. CBDT’s AI-driven Project Insight is selecting cases for scrutiny algorithmically within weeks of ITR filing.

How a Tax Notice Becomes a Financial Crisis — The 8-Stage Escalation Path

Most companies receive their first CBDT communication as a Section 142(1) general enquiry and treat it as routine administration. By the time they engage specialist advisors, they are already at Stage 4 or 5 — with a deteriorating factual record and a compressed appeal timeline. Understanding the escalation pathway is the first step to intercepting it early.

①

Section 142(1) — General Inquiry Notice

CBDT requests documents, books of account, or clarification. This is the earliest intervention point — and the most undervalued. Most companies route this to the accounts team. A specialist review at this stage resolves up to 70% of cases before they escalate further.

②

Section 143(2) — Scrutiny Notice

The return has been selected for detailed assessment. Structured hearings, document submissions, and mandatory response timelines now apply. This triggers the formal assessment proceeding — the stage where the quality of your documentation and representation determines everything that follows.

③

Section 148A — Show Cause Before Reopening

CBDT believes income has escaped assessment in a prior year and is proposing to reopen it. The taxpayer has 7–30 days (depending on the notice) to show cause why reassessment should not proceed. The response to this notice is the most consequential single document in the entire litigation pathway. A legally precise, evidentially supported response can stop the reassessment entirely.

④

Section 148 — Reassessment Order / Notice

The case is formally reopened. The Assessing Officer now has authority to examine all aspects of the year’s return — not just the originally alleged issue. This is where most cases significantly expand in scope, with additional disallowances and adjustments added beyond the original notice allegation.

⑤

Assessment Order + Section 156 Demand Notice

The AO passes an assessment order raising a demand. The taxpayer has 30 days to pay the demand or appeal to CIT(A). Failure to respond triggers penalty proceedings, coercive recovery action (attachment of bank accounts), and interest compounding at 1% per month on the full demand.

⑥

CIT(A) — First Appeal

Must be filed within 30 days of the assessment order. This is the most critical stage for building the appellate record — evidence and arguments not presented at CIT(A) are significantly harder to introduce at ITAT. Average disposal time: 18–36 months. Relief rate for well-represented taxpayers: 40–60%.

⑦

ITAT — Income Tax Appellate Tribunal

The second appeal — against the CIT(A) order. Over 5.4 lakh cases pending at ITAT as of March 2026. Average disposal time: 3–5 additional years. Advisory fees at ITAT stage: ₹15–40 lakh per matter depending on complexity. Requires specialist tax litigation counsel — not the filing CA.

⑧

High Court / Supreme Court

Only on substantial questions of law. Extremely expensive, extremely slow, and extremely rare — reserved for matters of significant value or legal principle. The company that reaches this stage typically has 8–12 years and ₹60–120 lakh in advisory fees already deployed. This outcome is almost always preventable at Stage 1 or 2 with the right advisory.

The critical insight on escalation: The company that engages specialist tax litigation advisory at Stage 1 (Section 142(1)) resolves the majority of cases before Stage 4 at a fraction of the cost. The company that first engages specialists at Stage 5 (after the assessment order) faces a demand with interest already accrued, an assessment record built entirely by the other side, and an appeal window that may already be narrowing. Every stage you wait to engage the right advisory costs you more — in fees, in interest, and in the quality of your factual position.

Have you just received a notice under Section 142(1), 143(2), 148, or 148A of the Income Tax Act — and you’re not sure whether to respond through your existing CA firm or engage specialist litigation counsel? The way you respond in the first 15–30 days sets the entire trajectory of your case. A factually incomplete or legally imprecise first response closes evidentiary doors that cannot be reopened on appeal — even at ITAT.

Let our Tax Litigation & Assessment Response team review your notice immediately, assess your exposure, and draft a response that protects your position — before the deadline. Click here for an immediate notice review or call us directly at +91-9953572838

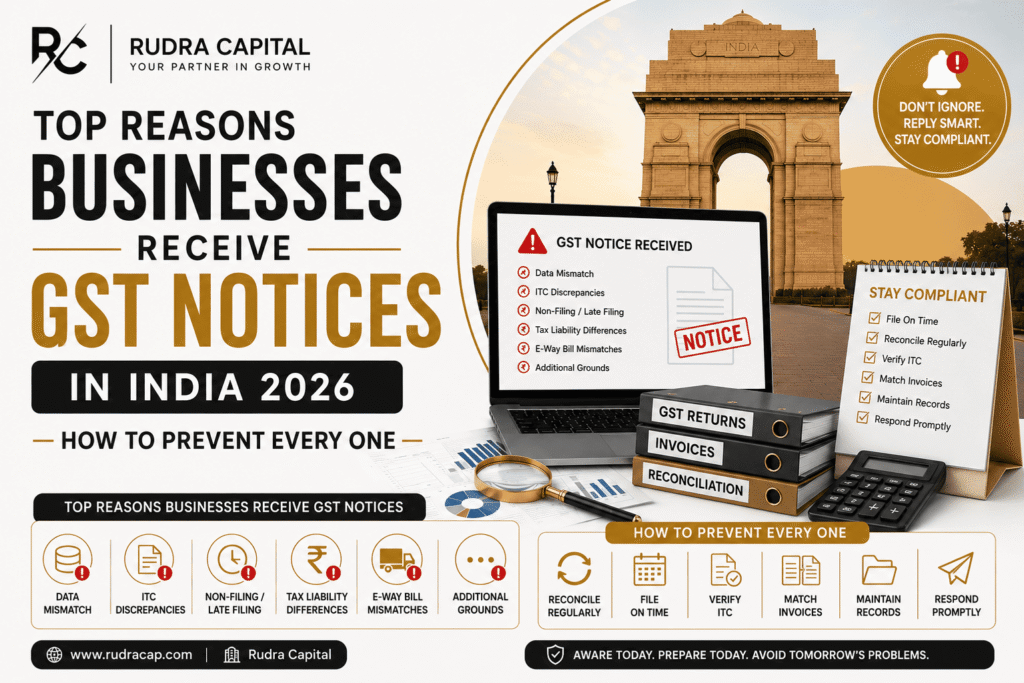

The 10 Most Common Notice Triggers CBDT Is Using Right Now in 2026

CBDT’s Project Insight — India’s AI-powered return analysis system — processes filed income tax returns and cross-references them against GST filings, bank transaction reports (SFT under Section 285BA), property registrations, import-export data, and social media for lifestyle indicators. The algorithm identifies specific patterns and automatically queues cases for scrutiny. These are the 10 patterns most commonly triggering notices in 2025-26:

- Cash purchases from vendors with no GST compliance history. Any significant cash purchase from a vendor not filing GSTR-1/3B is an automatic Project Insight flag. The algorithm identifies the mismatch within weeks of ITR filing.

- Related-party loans at below-market interest rates or unsecured loans from group entities. Section 2(22)(e) deemed dividend provisions and arm’s length interest scrutiny on shareholder loans are among CBDT’s top 5 adjustment grounds in corporate assessments for FY 2022-23 to 2024-25.

- Unexplained credit entries in bank statements — particularly entries not matching invoiced income. CBDT receives bank SFT data under Section 285BA from all scheduled banks. Credit entries above ₹50 lakh that don’t reconcile to ITR-declared income are flagged automatically.

- Revenue figures in the ITR and GSTR-1 that do not reconcile within 1%. CBDT now mandatorily cross-references these two data points. A ₹5 crore turnover divergence between your ITR and your GSTR-1 will generate a scrutiny notice within the current assessment year in most jurisdictions.

- High deduction claims under Sections 80IC, 80IB, 80IE, or 10AA without contemporaneous supporting documentation. Manufacturing companies in special economic zones and hill-area manufacturing exemption zones are a specific Project Insight priority for AY 2023-24 onwards.

- Share capital or share premium received from entities with no credible financial profile — Section 56(2)(viib) scrutiny. Closely-held companies that received funding at a premium from investors whose own financial statements show inadequate net worth are a consistently high scrutiny category.

- TDS short-deductions identified through Form 26AS cross-referencing. CBDT’s system now automatically reconciles vendor-side TDS certificates (Form 16A) with buyer-side deduction records. Any gap triggers both a TDS intimation under Section 200A and an income tax query on the disallowance risk under Section 40(a)(ia).

- Property transactions where stamp duty value significantly exceeds the declared consideration — Section 50C and 56(2)(x). Property registrations are shared with CBDT automatically. A ₹3 crore property bought at ₹1.8 crore declared consideration, with a stamp duty value of ₹3.2 crore, generates an automatic notice on the ₹1.4 crore gap.

- Foreign remittances and overseas payments not matched to inward service receipts or documented business purpose. CBDT receives bank remittance data and cross-references foreign outward remittances with Form 15CA/15CB filings and TRC documentation.

- Virtual Digital Asset (cryptocurrency) transactions not reported or inconsistently reported under Section 115BBH. Exchange-level data is now being collected by CBDT. VDA transactions above ₹10 lakh that are either absent from the ITR or inconsistently reported generate automatic scrutiny queue entry in 2025-26 assessments.

The TRUE Cost of Tax Litigation — What the Demand Amount Doesn’t Tell You

The most dangerous calculation a CFO makes is comparing the demand amount to the estimated litigation cost. This is the wrong comparison — because the demand amount is only the beginning. Here is the true, all-in cost of a ₹10 crore demand that runs from assessment to ITAT over four years:

| COST COMPONENT | Estimated Amount | BASIS |

|---|---|---|

| Tax demand under assessment order | ₹10.00 Cr | 20% deposited to maintain appeal; balance stayed |

| Interest under Sections 234B/C from original due date to resolution (4 years) | ₹4.80 Cr | 1% per month × 48 months on ₹10 Cr |

| Penalty under Section 270A (under-reporting — 50%) | ₹2.50 Cr | 50% of tax evaded — minimum penalty if contested |

| Advisory and legal fees (assessment → CIT(A) → ITAT) | ₹55 lakh | ₹8L at assessment + ₹12L at CIT(A) + ₹35L at ITAT |

| Cost of capital on ₹2 Cr demand deposit over 4 years (opportunity cost at 15%) | ₹1.20 Cr | 15% cost of capital × ₹2 Cr × 4 years |

| Senior management time diverted (CFO, Legal, Finance — 400 hours at ₹15,000/hour fully-loaded) | ₹60 lakh | Conservative estimate; complex cases exceed 600 hours |

| TOTAL ALL-IN COST ON A ₹10 CRORE DEMAND | ₹19.15 Cr+ | Nearly double the original demand — before outcome risk |

And this calculation assumes the assessment is contested and partially won at ITAT. If the demand is ultimately sustained in full — with a 200% misreporting penalty instead of 50% — the true cost of a ₹10 crore demand exceeds ₹32 crore inclusive of maximum penalties and four years of interest. Every rupee of that is potentially preventable through a proactive pre-litigation tax health framework implemented before the notice arrives.

Have you received a tax demand under Section 156 and assumed it is more efficient to pay and close the matter rather than contest it? Paying an incorrectly raised demand without appeal sets a precedent that the same position will be applied to every subsequent assessment year on the same issue — potentially creating a recurring liability. A demand that is wrong is cheaper to fight at CIT(A) than to accept. But the appeal window is only 30 days from the assessment order date.

Let our Tax Assessment & Appeal Specialist team review your demand order, assess whether it is legally sustainable, and tell you whether contesting it is the right financial decision — before the appeal window closes. Click here for a free demand review within 24 hours or call us directly at +91-9953572838

Seven Warning Signs Your Company Is Already on CBDT’s Radar

CBDT’s Project Insight doesn’t wait for companies to make mistakes before flagging them. It identifies risk patterns algorithmically — often within 60–90 days of ITR filing. These seven warning signs indicate that your company may already be in the scrutiny queue for the current or upcoming assessment year:

Warning Sign 1: Your ITR and GSTR-1 revenue figures do not reconcile within 1%

This is the single most common algorithmic trigger in 2025-26. CBDT cross-references these figures automatically. A ₹3–5 crore divergence between income tax declared turnover and GST declared turnover generates a mandatory scrutiny flag in most jurisdictions.

Warning Sign 2: You have related-party transactions above INR 5 crore without Transfer Pricing documentation

Related-party transactions — even between domestic group companies — are a scrutiny priority. The absence of TP documentation, combined with transactions at off-market terms, is a near-automatic adjustment ground in assessments of mid and large companies since AY 2023-24.

Warning Sign 3: Your bank statements show credits above INR 1 crore not directly traceable to invoiced income

CBDT receives SFT data from all scheduled banks under Section 285BA. Credit entries not matched to invoiced income — loan receipts, advances, capital infusion, or inter-company transfers — must be specifically explained in the context of the ITR filing. Unexplained credits above ₹1 crore are a Project Insight priority flag.

Warning Sign 4: You have purchased from vendors who have not filed their GST returns for two or more quarters

CBDT and GST authorities share data. Purchase deductions claimed in ITR from vendors with no GST filing history are flagged for disallowance — particularly where the vendor is not traceable at its registered address or has no credible business profile.

Warning Sign 5: Your company’s TDS deductions show gaps or non-deductions across multiple vendor categories

TDS gaps are a dual trigger: they generate a TDS intimation under Section 200A and simultaneously flag a potential Section 40(a)(ia) disallowance risk in the income tax assessment. A company with TDS compliance below 93% in any given quarter is in the active scrutiny selection zone for that year.

Warning Sign 6: You claimed exemption or deduction under Section 80IC/80IB/10AA in a prior year that is now being tested for ongoing eligibility

CBDT has made verification of continued eligibility for location-based and sector-based tax exemptions a specific AY 2024-25 scrutiny priority. Companies that claimed these deductions in earlier years are now being examined to verify that the conditions of eligibility are still met and that the requisite employment, investment, and production thresholds continue to be satisfied.

Warning Sign 7: You have never had an external pre-scrutiny tax health audit conducted — only relied on the filing CA

The CA who files your return has a compliance role — not a litigation defense role. Companies that have never had an independent specialist review their tax positions for scrutiny risk are, by definition, unaware of what their exposure looks like from CBDT’s perspective. Not knowing does not mean the risk doesn’t exist — it means the risk is unmanaged.

Do three or more of the seven warning signs above describe your company’s tax position in the last two to three assessment years? CBDT’s Project Insight processes return data algorithmically within 60–90 days of filing. If you tick three or more of these boxes, there is a high probability that your company is already in the scrutiny selection queue for AY 2024-25 or AY 2025-26. Don’t discover this through a notice.

Let our Pre-Scrutiny Tax Advisory team conduct a proactive exposure assessment — identifying your specific risk positions, quantifying your exposure, and implementing the documentation controls that reduce your scrutiny probability before CBDT gets there first. Click here to schedule a pre-scrutiny risk review or call us directly at +91-9953572838

CBDT’s 2026 Enforcement Priorities — What Is Actively Under the Microscope

Beyond the algorithmic scrutiny triggers, CBDT’s Directorate of Intelligence and Criminal Investigation (I&CI) and the Directorate of Transfer Pricing have issued specific sector and transaction priority notices for AY 2024-25 and AY 2025-26 assessments. These are the areas where manual scrutiny is actively being intensified in 2026:

- Family-held business and promoter group transactions: Unsecured loans between promoter entities, interest-free advances to subsidiaries, and share capital received from promoter-controlled entities at significant premiums are a specific scrutiny priority across all CBDT regional offices in 2025-26

- IT / ITES sector: Software companies claiming deductions under Section 10AA for SEZ units are being actively examined for employee headcount sufficiency, actual service export documentation, and separation of domestic vs. export revenue

- Real estate and construction: Project completion percentage methods, FSI-linked revenue recognition, and cash transactions in property sales — all under enhanced scrutiny with specific guidance issued to AOs in the western and southern regions

- Multinational enterprise PE and transfer pricing: As covered in our PE risk guide — CBDT’s international tax units are using CbCR data to identify MNCs with revenue and headcount in India but profits booked abroad. Service PE and Agency PE cases are in active assessment across technology, consulting, and engineering MNCs

- Healthcare and pharma: Hospitality-to-doctors expenses under Section 37 admissibility, distributor incentives under Section 194R TDS compliance, and clinical trial revenue recognition are all active scrutiny areas following specific CBDT instructions issued in Q3 FY 2025-26

- High-value capital gains: Long-term capital gains on listed securities, unlisted share sales through private transactions, and property sales where stamp value guidance rates have increased significantly post-COVID are being cross-verified against bank inward remittances and property registration data

- Crypto and virtual digital asset non-disclosure: Exchange-level VDA transaction data is now actively cross-referenced against ITR Schedule VDA disclosures. Under-reported or undisclosed VDA gains above ₹5 lakh are generating Section 148A notices within the same assessment year as filing

The Six-Pillar Pre-Litigation Defense Architecture — What Proactive Companies Do Differently

The companies that navigate CBDT scrutiny with the least financial and operational disruption are not the ones with the simplest tax positions — they are the ones with the most structured pre-litigation frameworks. Here is what a proactive tax defense architecture looks like in practice:

①

Annual External Tax Health Audit — Before Filing, Not After a Notice

An independent tax health audit conducted by specialist litigation advisors — not the filing CA — reviewing all material positions, deduction claims, related-party transactions, TDS compliance, and GST-ITR reconciliation before the return is filed. This is not a compliance review — it is a scrutiny risk review. The deliverable: a documented risk register with priority positions, supporting documentation requirements, and recommended pre-filing adjustments. Companies that do this annually reduce scrutiny selection probability by a measurable margin.

②

Documentation Control Room — At Time of Transaction, Not Time of Notice

Contemporaneous documentation of every material deduction, credit, related-party transaction, and exempt income claim — maintained at the time the transaction occurs, not assembled when the notice arrives. A response to a Section 142(1) notice supported by documents dated at the time of the transaction is 10x more credible than the same documents assembled after the notice. A Notice Response File — maintained throughout the year — is the single most important operational change a CFO can make in the finance function’s tax management process.

③

Written Notice Response Protocol — So the Accounts Team Never Responds Alone

A documented, board-approved protocol specifying: who within the organisation receives notices, who reviews them within 48 hours, which categories of notices are escalated to specialist advisors (and which CA firm is retained for that purpose), what the mandatory response drafting process is, and what information must never be volunteered in a response beyond what is specifically asked. This protocol, enforced consistently, prevents the most common and expensive notice response errors — excessive disclosure, unsubstantiated denials, and missed deadlines.

④

Clean ITR–GST–Books Reconciliation — Filed Before the Return, Not Discovered in Assessment

A mandatory pre-filing reconciliation of: ITR declared turnover vs. GSTR-1 turnover (within 1%), expenses claimed in ITR vs. GST input amounts (for verifiable categories), TDS certificates (Form 26AS) vs. income declared in ITR, and bank statement credits vs. ITR-declared income. This reconciliation, when completed and documented before filing, eliminates the most common algorithmic scrutiny triggers at source.

⑤

Litigation Reserve — Financial Provision for Known Risk Areas

A formal board-level provision for: estimated advisory costs for the coming year’s potential notice management, estimated demand deposit requirements if an open scrutiny assessment is resolved adversely, and penalty exposure from known uncertain tax positions. Companies without a litigation reserve discover their exposure only when the demand arrives — at which point the cash impact is immediate and undiversifiable. A properly calculated reserve should reflect 80th-percentile adverse outcomes on each known risk position.

⑥

Specialist Litigation Counsel — Retained Before the Notice, Not After

The best time to establish a relationship with a specialist tax litigation advisory firm is not when a notice arrives — it is before. A pre-retained litigation advisor who knows your business, has reviewed your tax positions, and has a documented briefing file for your company can respond to a Section 148A notice within 24–48 hours. A firm engaged cold on the day the notice arrives starts from zero — while the response deadline is already running.

A proactive pre-litigation tax health audit — conducted before any notice arrives — is the single highest-ROI action your finance team can take this financial year. It costs a fraction of what one litigation matter will consume in advisory fees, management time, interest, and penalty exposure. The analysis covers: ITR-GST reconciliation gaps, related-party transaction risk, TDS compliance gaps, deduction vulnerability, and notice-trigger indicators across the last two assessment years. But it only works before the notice. The moment a notice arrives, you are in reactive mode — and reactive is always more expensive.

Let our Pre-Litigation Tax Health Audit team conduct a comprehensive exposure review of your last two assessment years and build your Notice Response File before CBDT gets there first. Click here to schedule your pre-litigation tax audit or call us directly at +91-9953572838

How Rudra Capital Helps — Tax Litigation, Pre-Scrutiny Advisory, and Notice Management

Rudra Capital’s Tax Litigation and Pre-Scrutiny Advisory Practice is built around one mission: keeping our clients out of expensive, protracted tax disputes — and when a dispute is unavoidable, resolving it at the earliest possible stage with the strongest possible outcome. We work at both ends of the timeline: proactively, to prevent notices; and reactively, to defend against them with the full force of specialist representation.

Notice Response & Drafting

Emergency response drafting for all Section 131, 142(1), 143(2), 148A, and 148 notices — within 24–48 hours where required. We review, assess, and produce legally precise responses that protect your factual position for all subsequent stages.

Assessment Representation

Full representation before Assessing Officers in scrutiny assessments, reassessments, and transfer pricing assessments — including hearing management, document submission, and written submissions on legal positions.

CIT(A) Appeals

First appeal preparation, filing, and representation — the most critical stage for building a strong appellate record. We file within the 30-day window and manage every hearing through to order.

ITAT Litigation

Second appeal preparation, filing, and bench representation before ITAT. We work with specialist ITAT counsel where required for complex legal questions, and manage the matter end-to-end including departmental cross-appeals.

Penalty Mitigation Strategy

Specific advisory on converting 200% misreporting penalties to 50% under-reporting penalties, applying Vivad se Vishwas scheme benefits, and building the factual and legal record for penalty immunity under bona fide disclosure arguments.

Pre-Litigation Tax Health Audit

Annual pre-filing risk review covering ITR-GST reconciliation, related-party transaction scrutiny risk, TDS gap identification, deduction vulnerability assessment, and a prioritised litigation risk register — conducted before the return is filed, not after the notice arrives.

The companies that never end up in expensive tax litigation are not the ones with the simplest structures — they are the ones who treated litigation prevention as a year-round priority, not a post-notice emergency.

Rudra Capital has guided 120+ mid and large Indian companies through CBDT notices, scrutiny assessments, and ITAT appeals — and conducted 200+ pre-scrutiny tax health audits that caught material risks before they became demands. Whether you need a notice reviewed today or a proactive audit conducted this quarter, the first call is free.

+91-9953572838 | Book a Free Tax Litigation Risk Consultation →

+91-9953572838 | Book a Free Tax Litigation Risk Consultation →

Has your company never had a specialist tax health audit — relying only on the filing CA’s review — and you are not certain what your current scrutiny risk exposure looks like from CBDT’s perspective? Most mid and large companies that have never done this discover, in the audit’s first session, at least two to three material positions that are either undocumented, inconsistently reported across filings, or structurally exposed to the specific triggers CBDT is prioritising in 2025-26 and 2026-27 assessments.

Let our Pre-Scrutiny Tax Advisory team conduct your first proactive tax health audit — covering the last two assessment years, every material risk position, and a prioritised action plan for documentation and remediation. Click here to schedule your tax health audit or call us directly at +91-9953572838

FAQs — Tax Litigation and Notice Management in India 2026

Related reading: PE (Permanent Establishment) Risks for Global Businesses Operating in India 2026 · Top 10 Tax KPIs Every CFO Should Monitor Monthly in 2026 · Virtual CFO vs Traditional CA: Which Does Your Business Need in 2026? · Tax Litigation Advisory — Contact Rudra Capital